By Ashok Prasad, Founder, Niyyam

Published: June 2026

Introduction

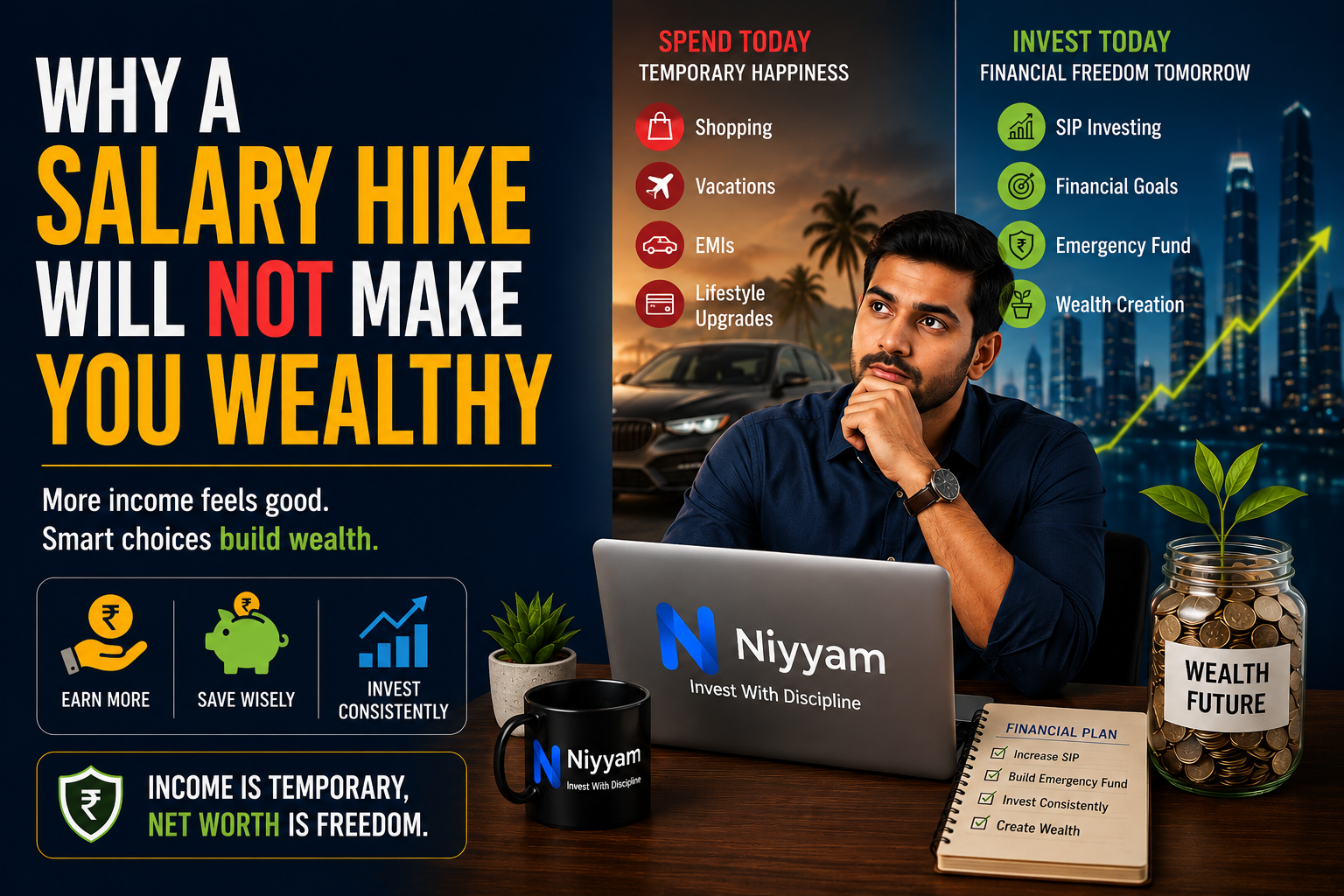

A salary hike will not make you wealthy. This statement may sound surprising, but it is one of the most important lessons in personal finance. Many professionals assume that higher income automatically leads to wealth creation, but the reality is very different.

A higher salary can certainly improve your quality of life. It can help you afford better education for your children, a more comfortable home, or a few well-deserved luxuries. However, there is one important truth that many people discover much later in life:

A higher salary does not automatically make you wealthy.

If salary hikes alone created wealth, every highly paid professional would become financially independent. Yet we often see people earning ₹2 lakh, ₹3 lakh, or even ₹5 lakh per month struggling with EMIs, credit card bills, and financial stress.

At the same time, there are individuals with far more modest incomes who quietly build substantial wealth over time.

The difference is not income.

The difference is what happens after the income is earned.

💡 Key Takeaways

- Salary hikes increase income but do not automatically increase wealth.

- Lifestyle inflation can consume most of a salary increase.

- Wealth is built through saving and investing, not merely earning.

- Increasing SIPs after every salary hike can significantly accelerate wealth creation.

- Net worth is a better measure of financial progress than monthly salary.

- Financial freedom comes from assets, not paychecks.

- Small financial decisions repeated over many years can create enormous differences in outcomes

𝗗𝗶𝗿𝗲𝗰𝘁 𝗔𝗻𝘀𝘄𝗲𝗿

A salary hike alone will not make you wealthy because wealth is determined by how much money you save, invest, and grow over time—not by how much you earn. If every salary increase is immediately spent on lifestyle upgrades, bigger EMIs, and discretionary expenses, your income may increase while your net worth remains stagnant. Long-term wealth is created when a portion of every salary hike is systematically invested in productive assets.

𝗪𝗵𝘆 𝗦𝗮𝗹𝗮𝗿𝘆 𝗛𝗶𝗸𝗲𝘀 𝗙𝗲𝗲𝗹 𝗦𝗼 𝗣𝗼𝘄𝗲𝗿𝗳𝘂𝗹

There is a psychological reason why salary hikes feel so rewarding.

When your monthly income increases:

- Your bank balance temporarily rises.

- You feel more secure.

- You gain confidence.

- You feel financially stronger.

Unfortunately, this feeling can create a false sense of financial progress.

Many people confuse increased income with increased wealth.

But income and wealth are not the same thing.

As we discussed in “The Day Your Salary Stops, Your Net Worth Starts Talking“, income helps you live, but net worth helps you survive. A growing salary is useful, but a growing net worth is what ultimately determines long-term financial security.

𝗧𝗵𝗲 𝗟𝗶𝗳𝗲𝘀𝘁𝘆𝗹𝗲 𝗜𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝗧𝗿𝗮𝗽

One of the biggest reasons salary hikes fail to create wealth is lifestyle inflation.

Lifestyle inflation occurs when expenses increase with every increase in income.

A typical example looks like this:

Year 1:

- Salary: ₹50,000

- Expenses: ₹35,000

- Savings: ₹15,000

Year 3:

- Salary: ₹70,000

- Expenses: ₹55,000

- Savings: ₹15,000

Year 5:

- Salary: ₹1,00,000

- Expenses: ₹85,000

- Savings: ₹15,000

Although income doubled, savings remained unchanged.

This is surprisingly common.

Many professionals upgrade:

- Their cars

- Their smartphones

- Their homes

- Their vacations

- Their dining habits

But forget to upgrade their investments.

𝗧𝗲𝘀𝘁 𝗖𝗮𝘀𝗲 𝟭: 𝗧𝗵𝗲 𝗦𝗽𝗲𝗻𝗱𝗲𝗿

Rahul starts his career earning ₹45,000 per month.

Over the next 10 years, his salary grows to ₹1,50,000 per month.

Every salary hike is used to improve his lifestyle.

His spending includes:

- A bigger car

- Expensive gadgets

- Frequent vacations

- Premium subscriptions

- Dining out regularly

By age 35:

- Salary: ₹1,50,000

- Investments: Minimal

- Emergency Fund: Insufficient

- Financial Stress: High

On paper, Rahul appears successful.

In reality, he remains financially vulnerable.

𝗧𝗲𝘀𝘁 𝗖𝗮𝘀𝗲 𝟮: 𝗧𝗵𝗲 𝗜𝗻𝘃𝗲𝘀𝘁𝗼𝗿

Priya also starts with a salary of ₹45,000 per month.

Like Rahul, her salary grows steadily.

However, she follows one simple rule:

Every salary hike must increase her SIP.

Whenever she receives a ₹10,000 increase:

- ₹5,000 goes towards investments.

- ₹3,000 improves her lifestyle.

- ₹2,000 strengthens her emergency fund.

By age 35:

- Salary: ₹1,50,000

- Large SIP portfolio

- Strong emergency fund

- Growing net worth

- Greater financial confidence

Both earned similar salaries.

Their financial outcomes are completely different.

𝗪𝗲𝗮𝗹𝘁𝗵 𝗜𝘀 𝗕𝘂𝗶𝗹𝘁 𝗢𝘂𝘁𝘀𝗶𝗱𝗲 𝗬𝗼𝘂𝗿 𝗦𝗮𝗹𝗮𝗿𝘆

Many people spend years negotiating higher salaries.

Very few spend the same energy building assets.

Wealth is created when money is converted into assets that can grow over time.

Examples include:

- Mutual Funds

- SIP Investments

- Retirement Portfolios

- Fixed Deposits

- Emergency Funds

- Real Estate

- Equity Investments

Your salary pays the bills.

Your assets create your future.

This is why successful investors focus on building assets rather than simply chasing higher income.

𝗧𝗵𝗲 𝗦𝗜𝗣 𝗔𝗱𝘃𝗮𝗻𝘁𝗮𝗴𝗲

One of the easiest ways to convert salary hikes into long-term wealth is through systematic investing.

Suppose you receive a salary hike of ₹10,000 per month.

You have two choices.

Choice 1

Spend the entire ₹10,000.

Result:

- Lifestyle improves.

- Wealth remains unchanged.

Choice 2

Invest ₹5,000 through SIP.

Result:

- Lifestyle improves moderately.

- Investments grow steadily.

- Net worth increases.

Over long periods, even small increases in SIP contributions can create substantial wealth.

This is one reason many investors struggle despite starting SIPs. As discussed in “Why Most Indians Start SIPs But Never Become Wealthy“, investing alone is not enough. Consistency and discipline matter far more than occasional investing.

𝗧𝗵𝗲 𝗘𝗺𝗲𝗿𝗴𝗲𝗻𝗰𝘆 𝗙𝘂𝗻𝗱 𝗠𝗼𝘀𝘁 𝗣𝗲𝗼𝗽𝗹𝗲 𝗙𝗼𝗿𝗴𝗲𝘁

Salary hikes often trigger spending decisions.

Rarely do they trigger emergency fund contributions.

This can become a serious problem during:

- Job loss

- Medical emergencies

- Economic slowdowns

- Family emergencies

Before upgrading your lifestyle, ask yourself a simple question:

“If my salary stopped tomorrow, how long could I survive?”

If you have not considered that question recently, you may find value in reading “If You Lose Your Job Tomorrow, How Many Months Can You Survive?“

An emergency fund may not feel exciting today, but it can become invaluable when life becomes unpredictable.

𝗧𝗵𝗲 𝗡𝗲𝘁 𝗪𝗼𝗿𝘁𝗵 𝗤𝘂𝗲𝘀𝘁𝗶𝗼𝗻

Most people track:

- Salary

- Bonus

- Increment

Few people track:

- Net worth

- Investments

- Asset growth

At the end of every year, ask yourself:

How much did my net worth increase?

That single question can reveal more about your financial progress than your salary slip ever will.

As explained in “The Day Your Salary Stops, Your Net Worth Starts Talking“, your financial resilience depends more on your accumulated assets than on your current income.

𝗔 𝗣𝗿𝗮𝗰𝘁𝗶𝗰𝗮𝗹 𝗥𝘂𝗹𝗲 𝗙𝗼𝗿 𝗘𝘃𝗲𝗿𝘆 𝗦𝗮𝗹𝗮𝗿𝘆 𝗛𝗶𝗸𝗲

Whenever you receive a salary hike, consider this framework:

50% Invest

- Increase SIP contributions

- Strengthen retirement planning

- Build long-term wealth

30% Enjoy

- Upgrade lifestyle reasonably

- Reward yourself

- Improve quality of life

20% Protect

- Build emergency funds

- Reduce debt

- Strengthen financial security

This simple formula ensures that every salary hike improves both your present and your future.

𝗪𝗵𝗮𝘁 𝗛𝗮𝗽𝗽𝗲𝗻𝘀 𝗔𝗳𝘁𝗲𝗿 𝟭𝟬 𝗬𝗲𝗮𝗿𝘀?

The real power of disciplined investing becomes visible over long periods.

Two people may earn identical salaries.

One spends every salary hike.

The other invests part of every salary hike.

After 10 years:

- One has a higher lifestyle.

- The other has a higher net worth.

After 20 years:

The difference can become life-changing.

This is why wealth creation is often less about earning more and more and more about making better decisions repeatedly.

𝗖𝗼𝗻𝗰𝗹𝘂𝘀𝗶𝗼𝗻

A salary hike is good news.

You should celebrate it.

You worked hard for it.

But remember:

A salary hike is an opportunity, not a guarantee.

The people who become wealthy are not necessarily those who earn the most.

They are often the people who consistently convert income into assets.

Every salary hike presents a choice.

Spend it all today.

Or invest part of it for tomorrow.

Your future net worth will largely depend on which choice you make repeatedly throughout your career.

Frequently Asked Questions (FAQs)

1. Does a salary hike automatically increase wealth?

No. Wealth increases when additional income is saved and invested rather than entirely spent.

2. What is lifestyle inflation?

Lifestyle inflation occurs when spending rises along with income, preventing meaningful wealth accumulation.

3. Should I increase my SIP after every salary hike?

Many investors find it beneficial to increase SIP contributions after salary hikes as part of a disciplined wealth-building strategy.

4. Why is net worth more important than salary?

Net worth reflects accumulated assets and financial strength, whereas salary reflects current income.

5. How much of a salary hike should be invested?

The exact amount depends on personal circumstances, but allocating a meaningful portion towards investments can support long-term wealth creation.

6. Why is an emergency fund important?

An emergency fund provides financial protection during unexpected events such as job loss, medical emergencies, or economic disruptions.

7. Can someone with a moderate salary become wealthy?

Yes. Consistent saving, disciplined investing, and long-term financial planning can help individuals build significant wealth over time.

Disclaimer

This article is intended solely for educational and informational purposes. It should not be construed as investment advice, financial advice, tax advice, or a recommendation to invest in any particular product or scheme.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully and consult a qualified financial advisor before making investment decisions.

Tech Margon Wealth Private Limited operates Niyyam.com.

AMFI Registered Mutual Fund Distributor

ARN: 360119

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply